The Secret(s) to Affording a Historic Home

Everyday citizens use three tools to live in great houses at little cost.

In Durham, North Carolina, they’re rebuilding the old historic neighborhoods frantically. The city has much to offer: a great downtown in the throws of rebirth, a large creative class, an active academic community, and, perhaps most importantly, 15 historic districts with a large stock of unique and affordable historic homes. Decades of downtown decline severely affected these neighborhoods. But now families are moving back to the city, which combines an urban lifestyle with the opportunity to restore a unique home. Those rediscovering residential life in central Durham want historic houses but are often unsure how to tackle a restoration project's specifics.

The number one question usually is: “Who can afford it?”

Well, almost anyone, actually. There’s much more to cost than the purchase price or monthly payment. There are financial benefits to owning any home in America and huge financial opportunities and incentives for those restoring historic houses in urban corridors. I‘ll walk through the great secrets to affording historic homes and show how many young couples, with real budgets and real lives, are affording landmark buildings for the same cost (or less) they might spend on a generic tract house in the suburbs.

Where people get stuck

As a restoration contractor, we’re used to seeing sticker shock. People are amazed at what historic homes with a quality restoration cost, both to rehab and to buy. Every weekend, buyers and tire-kickers drive around the old neighborhoods saying, “Can you believe what they’re asking for that one?”. Most never get closer to taking the plunge. But then the houses usually sell, and for their asking price. New owners were probably sold on the social or financial benefits of owning a historic home, probably both.

I’ll use Olivia and Trey Jones as our example couple. Like many, they were determined to buy a historic home but concerned about how to afford it.

Meet Olivia and Trey Jones .

Annual Income $100,000

Purchase Price $100,000

Rehab Costs $300,000

House Value $400,000

Mortgage $360,000

There are three major financial incentives open to historic homeowners in Durham: the mortgage interest deduction, historic rehabilitation tax credits, and the attached rental. Everyone gets the 1st incentive, but few, very few, take advantage of the latter 2. And therein lies the secret to affording a historic home.

mortgage interest deduction

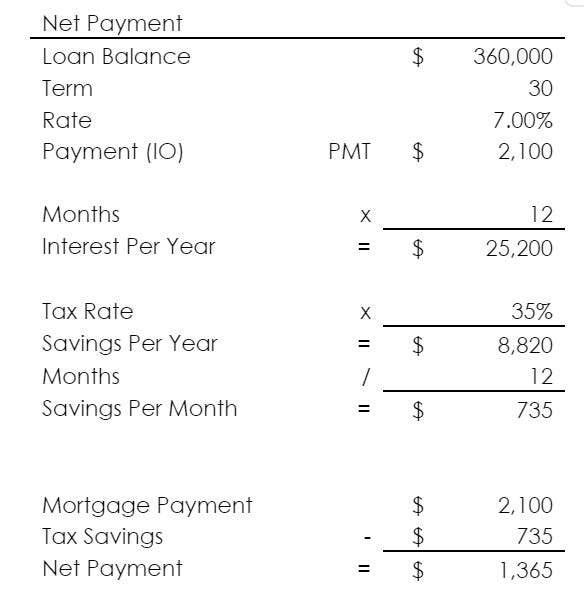

As a federal incentive to encourage homeownership, owners may deduct mortgage interest. Olivia and Trey have a $400,000 house with a 30-year interest-only mortgage for $360,000 at 7% (see note 1). Their monthly mortgage payment is $2,100. With 12 months, the Jones’ spend a whopping $25,200 in interest, 100% of which is deductible. As a deduction, this will lower their taxable income by $25,200 and (multiplied by their tax rate of 35%) create a real dollar savings of $8,820 annually. If we spread that savings out over 12 months, it equals $735 monthly. Thus, a $2100 interest-only mortgage payment is the net out-of-pocket equivalent of a $1365 ($2100-$735) rent payment.

It’s essential that realtors and homeowners understand this concept. It is the 1st great secret to owning any home, particularly a historic one.

historic rehabilitation tax credits

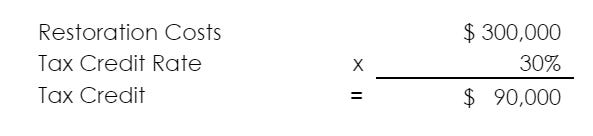

Durham is home to 15 neighborhoods listed on the National Register of Historic Places. At the time of the original publication, there was a 30% tax credit in North Carolina for restoring historic homes in these neighborhoods (see note 2). Essentially, when Olivia and Trey spent $300,000 to restore the dream home, the state gave them back $90,000 in credits to do so.

That’s a dollar-for-dollar credit, not, as is often wrongly assumed, a deduction. Since the Jones filed jointly and made $100,000 in income, and North Carolina has a 7% income tax, their state tax liability was $7000 ($100,000 x 7%). The tax credit wiped out their entire tax liability for that year. If they have already paid $ 7,000 in state income tax through their employer, they will receive a tax refund for $ 7,000, or $583 per month. The remaining credits carry forward, offsetting their income tax again the following year. It is the single most significant financial incentive available to homeowners and is highly underused.

Since 2002, 150-200 residential (non-income producing) tax credits have been processed statewide yearly. A disproportionate amount came from Durham, which tied Wake County for most originations in 2006. Historic tax credits are the 2nd great secret to owning a historic home.

attached rentals

ADUs are often as small as 400-800sf and can cover most of the primary homeowner’s mortgage.

I live and work between Duke’s East Campus and downtown Durham, a hotbed for intelligent grad students, adjunct faculty, and young creative class workers. Durham is not unlike other downtowns in this respect. University or not, downtowns from Denver to Asheville are flooded with good quality renters looking for good quality renting situations. Renters like living in secure homes in nice areas.

Attached dwellings (more technically “accessory dwellings”) come in various forms. These are not live-in roommates we’re suggesting. As separate housing, they all have private entrances, perhaps a basement apartment or a flat over a detached garage.

The attached apartment concept isn’t for everyone. I realize some couples dislike the idea of someone living in their house or at least need time to warm to the thought they hadn’t considered. Others might want all the space their large house offers. Many more might not have a house that allows for it.

The concept is straightforward for those who are open to the opportunity. If you rent a portion of your home, that income can offset your mortgage. Olivia and Trey, a young, childless couple, don’t yet need 3000sf. This allows them to afford a larger home, better quality finishes, or more thorough restoration. They have room to add to their family in the future while generating income from the space they don’t need today. It‘s like an addition-on-hold space that is paying for itself until required.

Trey and Olivia’s $400,000 house has an attached 2BR basement apartment. It’s the perfect setup for grad students, with a private entrance a few blocks from campus, a small kitchen and bath, excellent finishes, and even a tiny private garden. Near Duke, it rents easily for $800. And $800 covers nearly half their mortgage, even before considering any tax credits. Attached rentals are the 3rd great secret to affording a historic home.

the triple play

What happens when one combines all three secrets?

When Olivia and Trey found a project house they loved, they lost sleep over their ability to afford it. It needed work—a gut job-- with new HVAC, electric, plumbing, kitchens and bathrooms, framing, etc. It had a large unfinished private basement that could be finished into a great rec room or apartment. So they did the math. It would need $100/sf to restore, but it would qualify for tax credits and have a basement apartment to offset their mortgage.

Seriously?

It seems absurd to own such a house for the cost of a month’s groceries.

With a payment including taxes and insurance of $2275, their mortgage deduction yields a net payment of $1687. The tax credit offsets their entire tax liability to NC, giving them an extra $583 for a net payment of $1104. Finally, the rented basement gives them an additional $800 for a total all-inclusive payment of $304 per month.

Seriously?

It seems absurd to own such a house for the cost of a month’s groceries. Many say it’s too good to be true and leave it at that. But very real people are taking advantage of these very real mechanisms. In Durham alone, our clients and colleagues own a:

1700sf $250,000 bungalow with detached carriage house, main house owner-occupied, carriage apartment rented to student for $725. This leaves the owner with 1700sf and a $450/mo net payment.

2100sf $270,000 restored Victorian, lower level owner occupied, upper-level apartment rented to Duke Ph.D. for $600. This leaves the owner with 1300 sq ft and a net payment of $600/mo.

2200sf $300,000 restored bungalow, main house owner-occupied, basement studio rented at $700 leaves owner with 1600sf and a net payment of $600/mo. The contractor took tax credits.

4200sf $400,000 restored townhome, one owner-occupied, the other rented for $1250. Leaves owner with 2100sf and net payment of $700/mo.

3100sf $430,000 restored Victorian, main house owner-occupied, with attached apartment at $800/mo. Leaves owner with 2300sf and a net payment of $350/mo.,

5500sf $700,000 home, owner-occupied, with three rented units paying $3200/mo. The owner left with 2100sf and a net payment of $500/mo.

Attractive as these numbers are, few owners took advantage of tax credits. There are many variables that can affect the cost of rehabilitation expenditures and the potential financial benefits of owning a historic house. However, the fact remains that underutilized tools and mechanisms are available to owners (and potential owners) of historic homes.

conclusions

A common myth of historic homes is that they’re all museums – unattainable and expensive, meant to be looked at but not actually lived in – like your grandmother’s parlor. The fact is, Durham in particular (and the country in general) is blessed with a tremendous stock of historic homes are not museum pieces. They’re unique, offering different sizes and architectural styles, handcrafted by local tradespeople, and make fantastic modern-day homes. And, contrary to belief, they’re affordable. It is undoubtedly much more affordable if you are able to understand the mechanisms behind the true cost of ownership.

A house should, first and foremost, be a home: a place to raise a family. Only after that criterion is met should a house be looked upon as an investment. For years now, young couples have been flocking to the city to take advantage of the unique, high-quality old homes and old communities offer.

People ultimately buy (or don’t) because of these qualitative factors. Now, they can understand the financial benefits of owning a historic home yields as well.

ARTICLE NOTES

1 For simplicity’s sake, I’ve used an interest-only loan for our samples. If one chooses a traditional amortizing note, the numbers will change slightly, but the core points of this article do not. The principal is not deductible because it effectively pays you back by lowering your loan balance. Property taxes and insurance are also deductible and will be included in the overall analysis at the end of the article.

2 This essay was initially published in 2007. North Carolina’s tax credit incentives have changed since publishing. While still substantial, they are not as helpful as this article implies. Check with your local SHPO for current standards.